Secret Inflation

The secret behind inflation is one of the keys to understanding our broken world. And I believe that there is, really, a secret...

This is the first in a three-part series of long essays about what’s wrong with the world… Thank you all for following along, and thank you for letting me know what you think!

-Rob

The prices of sandwiches and underwear are going up rapidly and people are freaking out. Inflation! It seems to have come out of nowhere. Maybe it’s a post-Covid thing, or maybe caused by the war in Ukraine. Nobody really knows, actually, but fixing it has become the top priority of politicians everywhere.

I know this is a technical and boring topic in general, but I am convinced that the secret behind inflation is one of the keys to understanding our broken world. And I believe that there is, really, a secret, a truth that has been artificially hidden for years. Follow me for a minute here…

1. The price of startups has gone up too quickly

I’ll begin in the startup world, where I spend my workdays. About twelve years ago, after the financial crisis of 2008, something strange happened: the price of startups started to go up, and up, and up.

The price of startups – called their valuation – had been pretty stable for a decade. Rewind to 2002, after the “dotcom bubble” had burst. Let’s say you were an entrepreneur with a great idea. You spend a year or two working full-time to develop the concept, recruit an early team, build a prototype. At that point, your company would likely be valued between $3M and $4M in a Seed financing round, when you first tried to raise money from investors. (I’m talking here about startups in Silicon Valley, London or Paris; the numbers were lower outside of the big hubs).

In 2010, nearly a decade later, there were many more startups and more media frenzy around startup culture, yet the prices were relatively stable. If you started a company and raised Seed financing in 2010, you could still hope for a valuation around $3M to $4M.

Then something strange happened after 2010: the prices started to rise dramatically. In 2016, a startup in the same situation was valued at $5 or $6M, almost double. Today, in 2022, if you start a tech company in SF or Paris and develop your concept for a year or two, you can expect a valuation of your company around $10M in a Seed financing round. After a decade of stability until 2010, the price of early-stage startups has increased about 3x in the past 12 years, about 10-12% per year.

There is an obvious question to ask: has the underlying value of startups changed that much? Maybe startups have become more valuable to our societies as we realize how important they are to the economy. Maybe. But I am skeptical. That increase in perceived value wouldn’t explain a 3x increase in price, would it? And why did the increase only start in 2010, after the financial crisis, and not before?

Some suggest that the nomenclature has changed, that “Seed financing” used to be the first investment in a concept, but it’s been replaced by “Pre-Seed financing” which is essentially the same thing, and now “Seed” is the second investment a year or two later, so naturally the prices are higher. There is some truth to this explanation, too, but anyone in the industry can tell you that prices have obviously gone way up for startups at the same phase of development. The shifting labels does not explain it all.

The increase in the price of startups seems more simple and mechanical to me: there was just a lot more money in the investor community, billions and billions of extra dollars in their accounts, so the price of the limited supply of things they wanted to buy – in this case, shares of startups – went way up.

Maybe this was inflation, starting in 2010.

2. A quick definition of inflation: it’s not a measure of prices

This is a good moment in the argument to say what inflation actually is, because it can be a confusing concept. Sometimes inflation is defined as when prices go up, but that’s not quite right. Inflation is actually about the value of money itself.

Money is, of course, just a fiction, a way to represent the things that have real value in our world. Think about all the valuable things in our societies: the objects we possess, our homes and buildings and cars, the tools we use to work, our jewelry and clothes… but also abstract things like our working hours, the knowledge that we have, the brilliant inventions written up as patents. All of those things are valuable, and you can imagine that as a society, we have some total quantity of value when you add it all up.

If there are, let’s say, a trillion dollars (or euros) of money circulating out there in the world, and that’s supposed to represent this total quantity of all of the valuable things in the world, then each dollar is actually worth one trillionth of the real value in our world. That’s the value of a dollar.

And here’s where we can define inflation: if you suddenly increase the amount of money in circulation, let’s say to two trillion dollars, well, the amount of actual value in the world – what that quantity of money represents – stays the same. So each dollar is now worth half of what it used to be. The worth of dollars has gone down, because the amount of money in circulation has grown too fast, faster than the growth in actual underlying value. That is inflation, when the value of our money decreases because there’s too much of it in circulation.

When that happens, the prices of things will go up as a direct consequence. In the example I just gave, if money’s value is cut in half, then the price of a sandwich will double, because the sandwich itself has the same fundamental value to us.

(And I should pause here to acknowledge that this explanation is super super simplified, for many reasons. Real underlying value can be subjective, of course. And there is plenty of actual value in our societies that is not represented, or underrepresented, by money, like untouched nature and parents taking care of children and many other blind spots in our overly-financialized world. I will return to these points later, but for now the simplification is useful.)

3. It certainly seems like there’s 3.5% of unexplained annual inflation in financial markets

So maybe that’s what explains, partially, the increase in the price of startups since 2010. There was just more money around, the money supply grew too fast, so each dollar/euro was worth less, so the prices went up.

Something similar happened to prices of companies in the stock market. By one measure of value called the Shiller P/E ratio, it seems like the prices of stocks over the past 12 years, from 2010 until the recent mini-crash in 2022, increased by 50% more than would be justified by their increase in profits plus official statistics about inflation. That averages out to about 3.5% per year of unexplained increase in price (what Shiller, the Nobel-winning economist who first proposed the measure, famously attributes to his great phrase, irrational exuberance.)

That number, 3.5% per year of unexplained increase in prices, is pretty interesting in the case of startup valuations. It would suggest that the price increases of 10-12% per year for startups is partially due to an increase in the actual societal value of startups; partially due to the changing nomenclature of what we call a “Seed” round; partially due to the officially-measured inflation of 1-2% per year. Maybe, if we add all those phenomena together, we could say that over the past 12 years it makes sense that the prices of startups have doubled.

But it doesn’t make sense that prices have tripled. The delta, the difference between doubling and tripling (which is about 3.5% per year over 12 years), is an excess price increase, perhaps due to an oversupply of money in the system. Perhaps due to a secret, unreported inflation.

4. So if there’s extra/secret inflation, why have most prices stayed low?

What’s going on? If this extra inflation really exists, why hasn’t it been impacting the lives of normal people? Why have the prices of underwear and sandwiches stayed more or less the same, until very recently?

I finally found the answer in a brilliant paper by my friend Attila Gajdics. He explains that yes, inflation has been increasing massively since 2010, after the financial crisis. But we’ve been measuring it in the wrong way, so we haven’t noticed.

We measure inflation by looking at the price of the things we buy – underwear and sandwiches, used cars and gasoline, college tuition. If prices go up too fast, then the government economists determine that the money supply has increased too quickly (so the value of each dollar/euro has gone down), and they publish this conclusion as the official inflation statistic. This statistic is hugely influential, because it sets the annual adjustments in retirement pensions, minimum wages, and many other salaries that are mechanically tied to the official inflation numbers.

So since prices were not increasing too quickly, the official inflation numbers stayed low.

Attila figured out the error of this approach to measuring inflation. He explains that during that same period, since 2010, the real production cost of everyday things has actually been going way down, due to globalization (I mean, offshoring manufacturing of things to low-wage countries) and technology advances. In reality, the price of your underwear should have decreased a lot, it should have become a lot cheaper. Why? Because the company making it moved production to Bangladesh where they pay people five-times less than the previous factory in your home country. Because the robots in the factory got a lot better so there’s less need for the people with wages in any case. Because the company stopped wasting money on inefficient newspaper ads and instead started spending less, for more customers, on Facebook and Google. Because the company making the underwear had better tools for accounting, and HR, and everything else which made them more efficient at headquarters.

The reason that prices of consumer-goods have seemed stable, despite the decrease in their production costs, is partially explained by increased corporate profits (the company kept the prices the same and pocketed the difference in cost), but also partially by this secret inflation. This is the crux of the argument and the brilliant insight. We thought that stable prices mean low inflation and also low productivity-gains. But actually stable prices could mean high productivity-gains and high inflation. There was no way to make this distinction in the official numbers.

So not only have we been underestimating inflation, we’ve also been underestimating the productivity gains (and cost decreases) of consumer goods.

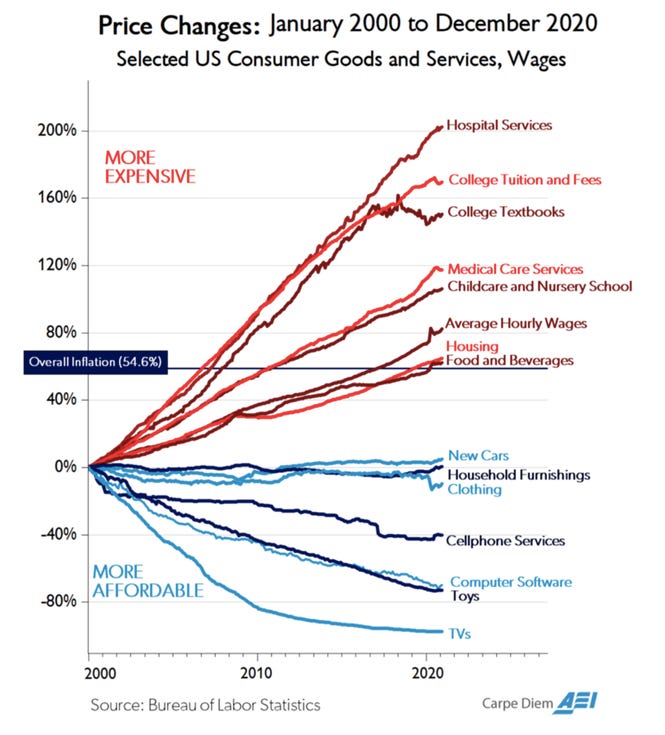

The parts of society where the secret inflation was not hidden were the domains where production costs didn’t get cheaper from offshoring and technology. Like, for instance, education, healthcare and childcare. Prices for those essential services have been going way up.

(That graph uses numbers from the US, but the story is similar in Europe.)

Perhaps these basic necessities of healthcare, education and childcare have become unaffordable for most people because of secret inflation, because our dollars and euros are worth less than they used to be, and the cost of delivering those services has not gone down. Since the official government statistics about inflation focus more heavily on the price of consumer goods, like TVs and cars, the official numbers have been under-representing the reality.

5. How did the secret inflation happen?

So this secret inflation has clearly been impacting the financial markets, but has been hidden from the statistics because the cost of consumer-goods has stayed stable.

The cause of this secret inflation is pretty obvious, actually, and awfully predictable. It happened because there was an oversupply of money in the system, compared to the actual need for money to represent value. That oversupply of money came from banks making tremendous amounts of loans with very-low interest rates. And those interest rates have been very-low because of the policy set by Central Banks after the financial crisis.

New money gets pumped into our societies in two ways: the government can just print new money, invent it from nothing, and then spend that money or give it away. Or, the second way, banks can loan new money, inventing it from nothing. It’s the second way that has been causing secret inflation.

We tend to think that a bank takes deposits from people and businesses, then uses that money it holds to make loans. That’s how it used to work. But not anymore, not in today’s modern, digitized economy. Today, a bank can hold $1M in deposits, and then it can decide to lend $10M to some business customer. All they have to do is open a computer, type “$10M” into a box, hit enter, and poof, that money now exists in the account of the business. The bank just invented that money. (OK, it is slightly more complex than that, but really not that much.)

Over the past 10 years, banks in the US have invented about $8T in new money in this way, by giving out loans with money that did not previously exist. In Europe it’s a similar story, which leads to tens of trillions of new dollars and euros invented since 2010. The amount of new money created by bank loans is much, much higher than the amount of money created by government printing & spending.

And this is where the story comes to interest rates, the most boring and confusing topic to appear in news headlines around the world. Central banks around the world moved the interest rates to zero in 2010. That meant that banks could loan money to people at super-low rates, basically for free.

Banks, as everyone knows, don’t lend money to just anyone. Try getting a loan when you have no savings and an inconsistent salary from freelance work: you’ll probably struggle, and even if you succeed, the loan will be small. Banks make loan decisions based on risk calculations, and of course it is safer to loan money to someone (or a company) that already has a lot of money. So if you’re a billionaire, it can be straightforward to get loans for additional billions.

And this is exactly what happened. Since stocks and startup-prices were going up by 10-12% every year, the financial elite was able to take out zero-interest loans, invest that money, and pocket the excess returns. Mark Cuban, one of the many billionaires who loves Twitter, tweeted a few years ago that the Central Banks of the world are pursuing “Universal Basic Income for rich people.” That’s about the shape of it.

6. So why are prices only going up now?

The price of sandwiches and underwear started to rise, rapidly, a few months ago. Why now?

It probably has a lot to do with the war in Ukraine and the consequent disruption to the world’s energy markets. Russia supplies a huge percentage of the world’s energy, in the form of oil and natural gas. Disrupting that supply caused the price of energy (and gasoline, and other kinds of fuel) to jump. Since fuel and energy are major inputs into the production of just about everything, businesses had to raise their prices to keep up. When the fisherman has to pay more for the diesel or gasoline to drive their boat, they need to raise the price of their fish to compensate.

As some prices started to go up, and the media started talking about inflation, it unleashed a vicious cycle. Businesses that had perhaps wanted to raise prices for a while suddenly saw their opportunity. As prices went up everywhere, workers demanded higher salaries. When the sandwich shop suddenly had to pay the sandwich-maker a higher salary, they had to increase their prices, too, and the cycle continued (and continues) to spin out of control.

Secret inflation had set the stage, and then Covid and the war in Ukraine provided the trigger. Now the media narrative has taken over to sustain the tornado.

Some analysts and politicians are suggesting, these days, that inflation is being caused by government spending – by the various covid recovery funds, or student loan forgiveness in the US. While it’s true that governments inventing new money does cause inflation, the amounts of money they create is a small fraction of the amount created by banks over the past decade. And the money created by the government, in recent cases, is intended for the masses, the people who are not benefiting from the free bank loans. So the politicians and pundits blaming new government spending are either ignorant of the mechanics of inflation, or disingenuous and trying to protect their relative advantage in an unfair system.

7. The implications of this seemingly-technical subject are just massive

Even with all this secret inflation in the past decade, wages have mostly stayed the same until recently. Except, that is, for those salaries most closely tied to the financial markets and the spigot of loans pumping new money into the world.

I suspect that the closer someone’s job is to financial capital, the more likely it is that their salary went up with secret inflation. The further away, the less likely. So someone who works in private equity or investment management saw their salary increase with the full (real plus secret) inflation. Likewise for startup executives (whose salaries are more tied to startup-financing than to actual startup performance), corporate executives who are compensated with stock, legal teams working most closely with financial investors, etc. The people following this full inflation curve probably represent about 5-10% of working adults.

The rest of the world, the 90-95% of people whose work is less connected to financial markets, did not see their salaries rise with the secret inflation, only with the reported inflation. And this means that in reality, their salaries have gone down, because each dollar and euro is worth less.

Perhaps this is why, even before the price-inflation of the past few months, “cost of living” (and “pouvoir d’achat” in France) were the most important political topics in most countries. People have noticed that life has gotten too expensive. It just hasn’t been clear why, and how to fix it.

This isn’t the typical story we hear about widening inequality, the rich getting richer and the poor getting poorer. The implications of secret inflation are that everyone is getting poorer.

If people in the mainstream feel like life is too expensive these days, it’s probably because they’re right, because their money is worth less than it used to be.

If a huge segment of society feels like they have been forgotten, and they see the elites as living in a separate universe (with purchasing-power that has not gone down), maybe it’s because they actually have gotten poorer, and no one has acknowledged it, and yes, the 5-10% of people who were already the richest and living in the big cities are, in fact, the only ones living in an alternate reality where life is not getting more expensive relative to their paychecks. I am not proposing this as the sole or main explanation of resurgent populism – which is a complex phenomenon – but it makes sense to me as one important ingredient.

Perhaps that’s why, in the past decade, it has become common wisdom in the startup world that it’s better to build a B2B startup than a B2C startup (unless, that is, you’re building a B2C startup for the highest-earning 5-10% of society whose wages are tied to the financial markets).

Disposable income for the mass-market is significantly lower than it was ten years ago.

There’s another important implication which is that productivity gains from technology have been higher than official measures indicate. There is an argument in the academic world about whether new technology is actually increasing productivity or whether growth has slowed. The insight about secret inflation indicates that productivity gains have not slowed, not at all.

In the next post I’ll write about how this secret inflation has impacted the parts of our societies that have not experienced productivity gains, especially the various activities involved in caring for people.

Really insightful and much appreciated! I definitely saw the startup valuations skyrocketing right around the 2010 recession; I wonder if there is a more direct connection between that and your observation about self-serving customer bases (both B2B and B2C). In 2010, partly to help recover from the financial crisis, there were many explicit tax credits for startup investment (eg see this overview of US state angel investment incentives https://www.cga.ct.gov/2010/rpt/2010-R-0376.htm) and with interest rates at zero, this further intensified the ROI of startup investment. This incentive loaded up startups with more cash, which then fueled a flywheel of both B2B services spending ("Process back-office transactions manually? Let's try this SAAS service instead?") and B2C ("I'm working late at my overcapitalized startup; let's order gourmet food delivery tonight"). Even the Cloud: In 2010 I distinctly remember pricing out this "AWS thing" which was way more expensive than we paid for bare metal servers, but once we raised our next round, my team was pretty adamant it was suddenly a good deal.

I don't know whether startups as both producers and consumers is enough to explain this effect but it feels like there's a strong, self-reinforcing component to your top 5-10% segment.

Thanks again!

Brilliant. All very true. As per Hayek’s 1976 book “The Denationalization of Money”. I slightly differ in that I believe governments and Central Banks are the main culprits, banks are just accessories to crime. As per the huge rise in FED and ECB balance sheet over the period. It’s “La planche à billets” foremost.